This spring, Louisiana voters will be asked to consider the most substantial change to the state’s constitution since it was adopted in 1974.

Amendment 2 on the March 29, 2025 statewide ballot is a proposed overhaul of the longest portion of the state’s foundational document, which deals with taxes and government spending. If approved by voters, it would enshrine a regressive tax system where the wealthiest people and corporations pay far lower overall tax rates than people with low incomes. It would eliminate constitutionally protected funds that provide ongoing funding for education and transportation programs, and make it harder for state policymakers to deal with the ups and downs of Louisiana’s economy.

It is likely to leave Louisiana with less revenue, at both the state and local levels, to pay for essential services that people and communities need in order to thrive.

This amendment is being presented to voters in language that is misleading, and which fails to capture the true extent of what voters are being asked to consider. It was passed as part of a rushed, 16-day special session where the Legislature also made wholesale changes to the state tax structure – cutting personal income and corporate taxes while raising the state sales tax to make up a part of the lost revenue.

The legislation revising Article VII spans 115 pages. The ballot language voters will see on the March 29 ballot was reduced to 91 words.

Do you support an amendment to revise Article VII of the Constitution of Louisiana including revisions to lower the maximum rate of income tax, increase income tax deductions for citizens over sixty-five, provide for a government growth limit, modify operation of certain constitutional funds, provide for property tax exemptions retaining the homestead exemption and exemption for religious organizations, provide a permanent teacher salary increase by requiring a surplus payment to teacher retirement debt, and make other modifications? (Amends Article VII, Sections 1 through 28; Adds Article VII, Sections 29 through 42)

Passing Amendment 2 would make it harder for our leaders to address the real problems that Louisiana faces. Understanding the ballot language and the more complex policy changes beneath it makes that clear.

Capping Personal Income Tax Rates

…including revisions to lower the maximum rate of income tax…

The current constitution includes a 4.75% cap on individual income tax rate. The proposed constitutional amendment would reduce the cap to 3.75%. Under the new state tax law that took effect in January, Louisianans pay a 3% flat rate on income above a certain threshold, so the lower constitutional cap would not affect what people currently pay in taxes.

Before the new tax law, Louisianans paid income tax based on graduated rates, meaning that as the income of individuals and families increased, slightly higher rates were applied to higher income. For a family filing jointly these rates ranged from 1.85% on taxable income up to $25,000 to a top rate of 4.25% on taxable income over $100,000.

Moving to a flat income tax is projected to cost the state $1.1 billion in lost revenue. Lawmakers offset this revenue loss by increasing the state sales tax rate to 5% through 2029, and broadening the list of goods and services that are subject to tax – making Louisiana’s combined state and local sales tax rate the highest in the nation. According to the Institute for Taxation and Economic Policy, this shift translates to a slight tax increase for the poorest Louisianans, while the richest 1% will receive a $15,431 tax cut. While the new sales tax rate is set to decrease by 0.25% in 2030, the effects on low-income households would be negligible.

Capping personal income tax rates as Amendment 2 proposes would make it more difficult, if not impossible, for state lawmakers to undo the harm they did with their tax swap last fall and would cement the state’s burdensome sky-high sales tax rates.

A tax system should be sufficient to meet the state’s needs and take into account an individual’s ability to pay. A progressive personal income tax that ties one’s rate directly to one’s income is a hallmark of a more equitable tax system by reserving the highest rates for the filers with the highest level of income, individuals who spend a far lower portion of their household income on basic necessities.

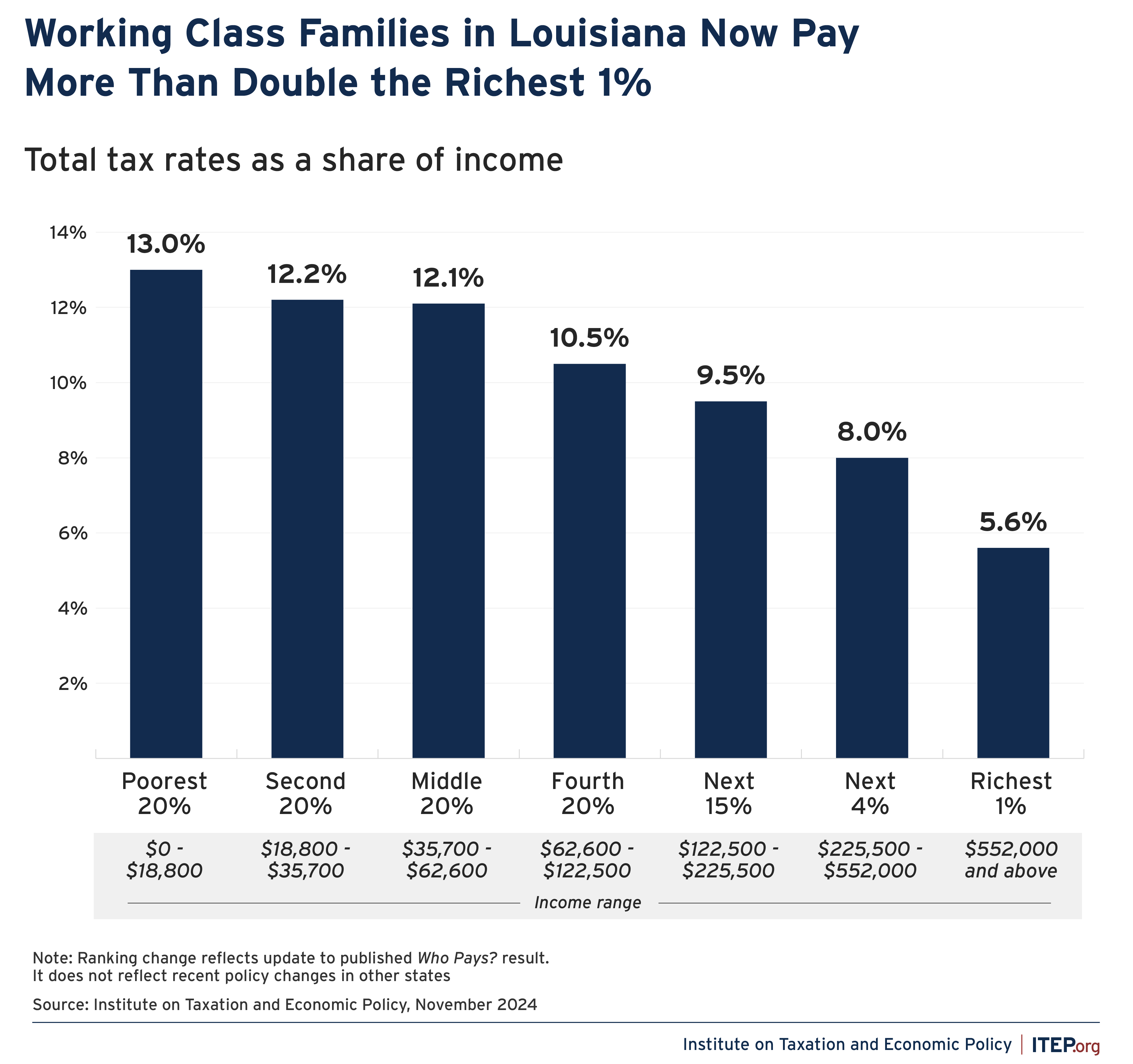

Louisiana’s tax system is upside down. Our overreliance on sales and use taxes translates to a tax system where the poorest among us pay 13% of their household income in state and local taxes, while those at the top of the income ladder pay only 5.6% – less than half the effective tax burden of people living below the poverty line.

{kind=link}

While a cap on personal income tax rates would not directly impact the state’s sales tax rates, lowering the cap in the constitution would make it more difficult to raise enough revenue to return to a more progressive graduated personal income structure.

Arbitrary Limits on State Spending

…provide for a government growth limit…

Amendment 2 would create a new Government Growth Limit, which could be the most dangerous and far-reaching aspect of this proposed constitutional amendment. It would create an artificial constraint on the state’s ability to fund state spending that is blind to the needs of citizens.

Louisiana already has a constitutional limit on how much state tax dollars can be spent each year. This “Expenditure Limit” is set annually using the percentage change in the personal income of Louisiana’s residents. The Legislature has the authority to increase or decrease the expenditure limit, and they have exercised that authority several times over the last 20 years.

The proposed Government Growth Limit would be a lower ceiling that gives legislators much less flexibility in funding new and ongoing programs, even when there is money available. The growth limit would be determined in the first quarter of the calendar year and would be calculated by a formula that averages state population change and the rate of inflation for ordinary goods and health care.

If state revenues exceed the growth limit, that extra money could still be spent, but only on “non-recurring” items and not ongoing expenses – even if the money is there to support the services from year to year. The language also severely limits the Legislature’s authority to change this new limit, unlike their authority with the expenditure limit.

This Government Growth Limit is not a novel idea. It is similar to the growth limit established in the Taxpayer Bill of Rights Colorado adopted in 1992. The people of Colorado learned the hard way that their formula could not keep up with the normal increase in the cost of maintaining state services and prevented new investments altogether. Using population growth failed to account for demographic shifts within the state’s population. It’s more expensive to provide essential services for senior citizens and school-age children than other populations. And the costs to provide education and other state services typically rise faster than the consumer goods tracked through CPI.

A government growth limit is predicated on the belief that the current state budget is adequate and the needs of the state’s citizens are being met – that status quo spending levels need only to be maintained to ensure all of the state’s citizens have the support they need to thrive.

That is not the case in Louisiana. Lawmakers of the future must have the ability to make sound decisions based on the needs of the moment and the resources at hand. Further, the growth limit as proposed in Amendment 2 would prevent those lawmakers from making the transformational investments in our state needed to address the chronically unmet needs of our citizens.

Raiding Special Funds

…modify operation of certain constitutional funds…

This proposed constitutional rewrite and its statutory companions would eliminate or alter more than half of the special funds that currently reside in Article VII. Some of those accounts would be eliminated, freeing the monies within for other purposes. Other funds would be removed from the state constitution, but retained in statute, allowing the funds to be altered in future legislative sessions.

The most significant of the proposed changes would eliminate the Revenue Stabilization Trust Fund (RSF) while raising the cap of the Budget Stabilization Fund (BSF), also known as the Rainy Day Fund. The Revenue Stabilization Trust Fund is a relatively new state savings account, created by a statewide vote nearly a decade ago, that was designed to mitigate the volatility of corporate and mineral tax collections by collecting “excess” tax revenue during boom years. Legislators could tap the account in lean years, or to fund capital construction projects such as roads, bridges or other public infrastructure.

Currently the RSF contains about $2.76 billion, while the Rainy Day Fund has $1.1 billion stashed away.

Amendment 2 and its statutory companions would transfer $1.75 billion from the RSF into the Rainy Day Fund, which would then hit its new cap of $2.8 billion. The remaining $1 billion from the RSF funds would be used to offset the loss of corporate tax revenue caused by tax cuts made in the special session, and to provide one-time payments to parishes that agree to permanently eliminate revenue they receive from a property tax on corporate inventory. The RSF would be closed in 2027, and anything left in the account would be swept into the state general fund.

This is an irresponsible use of one-time dollars on recurring expenses to obscure the fiscal impact of the corporate tax cuts the Legislature pushed through last fall. Further, by eliminating the Revenue Stabilization Trust Fund and spending the balance, the state is reducing its emergency savings by $1.1 billion.

Louisiana needs to reevaluate the role of statutory and constitutional dedications. But this amendment is the wrong approach, as it reduces the state’s emergency reserves and eliminates a source of funding for capital construction projects.

Cannibalizing Education Funding

…provide a permanent teacher salary increase by requiring a surplus payment to teacher retirement debt…

Public school teachers in Louisiana are underpaid. With Amendment 2, they would still be getting the same pay they currently receive; the money would just come from a different pot.

Amendment 2 would eliminate three state trust funds that were created by voters to safeguard windfall revenue the state received from offshore oil and gas production and the global settlement with tobacco companies. Currently, the interest from these funds is spent in support of education programs – from Pre-K through college.

The amendment would eliminate the Louisiana Quality Education Trust Fund, the Louisiana Education Quality Support Fund and the Education Excellence Fund. Each year the investment earnings of these funds are distributed to provide services at all education levels in the state. In the current fiscal year, $64 million of these funds’ investment earnings were appropriated to such programs.

The three trust funds hold approximately $2 billion, which would be used for a one-time payment to the Teachers’ Retirement System of Louisiana (TRSL) to be applied to retirement system debt (Louisiana Legislative Fiscal Office 2024). That debt is currently paid through regular employer contributions by all employers who participate in TRSL. Pre-paying that debt will reduce the costs that local school systems have to pay for retirement, which frees up money that local school districts are expected to use to provide a $2,000 pay raise for teachers and a $1,000 raise for school support personnel.

Funds eliminated by Constitutional Amendment 2 provide $64 million in essential education funding in FY25

| Recipient | Amount |

|---|---|

| Louisiana Quality Education Support Fund – BESE | $20,500,000 |

| Louisiana Quality Education Support Fund – Board of Regents | $20,080,000 |

| Education Excellence Fund | $23,677,163 |

| Total | $64,257,163 |

Source: Internal calculations, Act 4 of the 2024 Regular Session, and the Education Excellence Fund Report, LDOE, presented to the House Education committee on December 12, 2024.

In reality, the pay raises from local school boards will simply replace annual stipends that teachers have received from the state the past two years. In both the 2023 and 2024 legislative sessions, teachers and support staff received $2,000 and $1,000 pay stipends, respectively. These stipends were not part of teacher and support worker salary schedules, and districts had flexibility in how they paid the stipend.

Backers of the constitutional amendment claim that the payment to TRSL and the requirement that districts pay staff with the savings will ensure that teachers and support staff receive a permanent pay raise.

Aside from its complexity, the language in the amendment does not guarantee a pay raise. Teachers and support staff would not see any more money in their paychecks, they just would not lose the temporary pay bump lawmakers provided. In fact, companion legislation acknowledges that not all districts will see the savings needed to make the stipend permanent. Further, the scheme could neglect charter school faculty and staff, who typically are not included in the TRSL.

Lawmakers can, and should, give all public school teachers a permanent pay raise through the Minimum Foundation Program – the state’s K-12 education funding formula. Doing so would require lawmakers to make a recurring investment in public education – the kind of investment that would be more difficult if the growth limit proposed elsewhere in this amendment were to take effect.

Everything Else

…and make other modifications?

The four words “and make other modifications” are all that’s left to account for the myriad changes Amendment 2 would make to our state constitution and the dozens of sections of statues that would take effect if approved by voters this spring.

Those changes include imposing a supermajority requirement for any new tax credits, making significant changes to how the state’s severance tax is applied to natural resources and how it is paid out to local governments, and several measures that take taxing authority from local governments’ and give it to the state Legislature.

It is important to note that all of this was ostensibly proposed to streamline our state’s constitution. Instead, the drafters of this amendment took the longest and most complicated article of our state’s foundational document and made it longer and more complex. Article VII started with 28 sections, and if this Amendment passes it will have 42 – all in the name of simplicity.

It is a disservice to Louisiana voters to ask them to consider such a wide range of changes with one single ballot measure, especially when considering the way this was rushed through the legislature.

References

Butkus, Neva. 2024. “Louisiana Lawmakers Pass Deeply Regressive Tax Plan.” Institute for Taxation and Economic Policy. https://itep.org/governor-jeff-landry-louisiana-lawmakers-regressive-tax-plan/.

Center on Budget and Policy Priorities. 2019. “Policy Basics: Taxpayer Bill of Rights (TABOR).” Center on Budget and Policy Priorities. https://www.cbpp.org/sites/default/files/atoms/files/policybasics-tabor_0.pdf.

Louisiana Legislative Fiscal Office and Julie Silva. 2024. “Fiscal Note Act 8 of the 2024 Third Extraordinary Session.” https://legis.la.gov/legis/ViewDocument.aspx?d=1391446.